Q1 earnings from Home Depot, Lowe’s, and Walmart reinforced something important about the current retail environment:

Consumers haven’t stopped spending on the home. But they are becoming much more selective about how they spend. That distinction matters. Because while larger discretionary remodel activity continues slowing under pressure from higher rates, inflation, and softer housing turnover, spending tied to maintenance, replacement, refresh, convenience, and smaller DIY behavior appears much more resilient. And increasingly, those purchases may not all be flowing through traditional home improvement retail.

The Quarter Wasn’t About Growth. It Was About Traffic.

At a surface level, Q1 earnings across retail looked relatively stable:

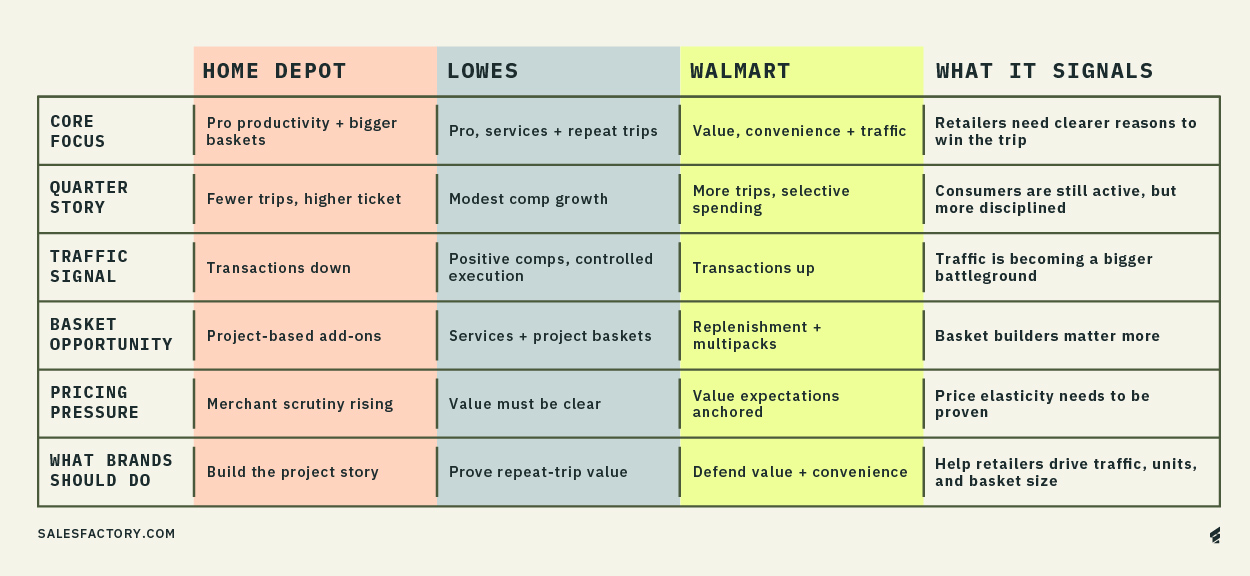

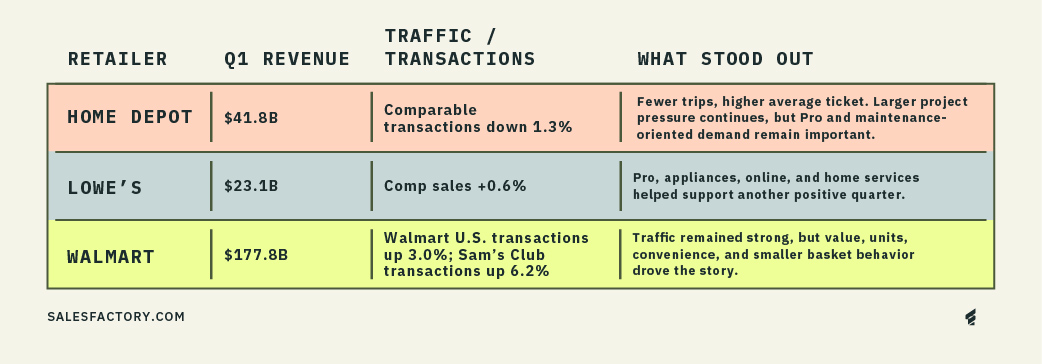

Home Depot reported:

- $41.8B in revenue

- +0.6% comparable sales growth

- transactions down 1.3%

- continued pressure around larger discretionary projects

Lowe’s reported:

- $23.1B in revenue

- +0.6% comparable sales growth

- strength in Pro, appliances, online, and home services

Walmart reported:

- $177.8B in revenue

- Walmart U.S. transactions up 3.0%

- continued market share gains tied to value and convenience behavior

None of the retailers sounded alarmed. But the tone across all three earnings releases was disciplined. Execution-focused. Controlled. The biggest signal from the quarter wasn’t explosive growth. It was how aggressively retailers are fighting for traffic, frequency, basket size, repeat visits, and value perception.

That matters because softer traffic in home improvement retail creates pressure elsewhere in the business. If fewer shoppers are coming in for large remodel projects, retailers increasingly need basket builders, project-based purchases, add-on items, replenishment behavior, and impulse-friendly merchandising to offset the pressure. That changes what merchants prioritize.

Big Projects Slowed. Smaller Projects Didn’t.

The environment still appears challenging for larger remodels, financing-heavy projects, housing-turnover-dependent categories, and discretionary big-ticket spend. But categories tied to maintenance, repair, replacement, paint, seasonal, outdoor refresh, organization, smaller DIY projects continue holding up better.

That’s an important distinction. Consumers are still investing in their homes. They’re simply becoming more cautious about financing, project scale, timing, and overall basket commitment. And that creates a very different retail environment than the industry operated in over the last several years. The consumer behavior is shifting from rebuild to maintain, remodel to refresh, and destination project trips to convenience-oriented replenishment behavior.

Tax Return Season Didn’t Fully Rescue Big-Ticket Demand

Another important signal from Q1:

Even with tax return cashflow entering the market, larger discretionary home improvement purchases still appeared pressured. That matters because Q1 is typically one of the stronger seasonal windows for project starts, deferred purchases, appliance replacement, outdoor upgrades, and larger DIY activity.

This year, however, the earnings commentary across retail suggested consumers remained cautious around bigger financed projects despite the seasonal tailwind. Instead, shoppers appeared more willing to spend tax return dollars on maintenance, smaller refreshes, seasonal purchases, practical replacement items, and value-oriented household spending.

That creates an important watchout moving into Q2 and the back half of the year. Because if larger-ticket categories struggled even during tax return season, those categories may face additional pressure as that temporary cashflow tailwind fades. Especially in an environment where housing turnover remains soft, financing costs remain elevated, consumers continue prioritizing flexibility and value, and retailers are competing harder for traffic. That dynamic likely increases pressure on merchants to drive more trips, expand baskets, promote project-oriented purchasing, improve attachment selling, and scrutinize pricing more aggressively.

For brands, this reinforces the importance of value communication, basket-building opportunities, project merchandising, pricing elasticity planning, and promotional readiness as retailers work harder to stimulate demand in a slower-growth environment.

Walmart Is Now Competing For More Home-Related Spend

This is where Walmart becomes increasingly important to the story. Historically, many lower-ticket home purchases naturally flowed toward home centers. Today, those trips appear much more fragmented. Consumers increasingly purchase cleaning supplies, storage, organization, replacement items, outdoor accessories, small tools, paint accessories, and maintenance products through the same channels they already use for groceries, consumables, household replenishment, same-day delivery, and ecommerce convenience.

That creates a meaningful competitive shift. Not because Walmart suddenly replaces Home Depot or Lowe’s. But because consumers increasingly separate large project behavior from ongoing maintenance behavior.

And Walmart is structurally advantaged in the second category. Especially in an environment where convenience matters more, consumers remain value-sensitive, trips are consolidating, smaller baskets are increasing, and discretionary projects remain pressured. Walmart’s transaction growth this quarter reinforced that shoppers are still actively spending, but increasingly through smaller, value-oriented purchasing behavior.

Pricing Pressure Is About To Intensify

This may be one of the most important implications for brands moving into the second half of the year. Traffic pressure changes merchant behavior. When traffic softens, retailers become more aggressive around pricing scrutiny, promotional expectations, elasticity conversations, value communication, and basket expansion opportunities.

That means brands should expect tougher conversations around pricing increases, promotional support, pack architecture, margin expectations, and competitive pricing, especially inside categories tied to discretionary projects, premium positioning, and slower-turning inventory.

Retailers will increasingly prioritize products that help drive traffic, increase units, expand baskets, support project-based purchasing, and improve perceived value. The brands best positioned for this environment will likely be the ones that understand how to build basket-friendly assortments, project-driven merchandising, multipack opportunities, impulse add-ons, and clearer pricing stories before merchants force those conversations later.

What This Means For Brands

The biggest takeaway from Q1 earnings isn’t that consumers stopped spending. It’s that retailers are becoming more disciplined about how growth gets created. Traffic pressure, softer big-ticket demand, and more value-sensitive shoppers mean merchants are increasingly focused on basket expansion, trip-driving categories, promotional efficiency, pricing elasticity, value communication, and repeat purchase behavior.

That creates new pressure on brands. Retailers will increasingly prioritize products that help drive store visits, build baskets, support projects, improve conversion, justify pricing, and create add-on purchase opportunities. Especially in categories where traffic has slowed, large projects remain pressured, and consumers are delaying discretionary spend.

That doesn’t mean retailers are abandoning bigger projects or premium categories. But it does mean brands may need to work harder to explain why the product deserves its price, how it supports the overall basket, what role it plays in a project, and how it helps retailers drive profitable trips. The brands best positioned for the second half of the year will likely be the ones that make purchasing easier, value clearer, and basket-building more natural.

Think project-based merchandising, multipacks, attachment selling, solution-oriented displays, stronger promotional architecture, and clearer packaging communication. Because in a slower-growth environment, retailers aren’t just looking for products that sell. They’re looking for products that help the entire trip become more productive.

Ready To Pressure-Test Your Pricing Strategy?

Sales Factory helps brands evaluate:

- pricing tolerance

- value perception

- competitive positioning

- shopper behavior

- retail channel vulnerability

- elasticity risk

before pricing pressure becomes a margin problem.